CITIZENS DEVELOPMENT BUSINESS FINANCE PLC

ANNUAL REPORT 2021/22

Operating environment and our response

Market drivers

By paying close attention to the environment in which we operate, we scan the horizon for risks and opportunities, and adapt our strategy accordingly. We also monitor trends in the behaviour of our customers to effectively meet their evolving needs. Especially at a time when our Nation is in crisis, we extend our support to rebuild our country by empowering aspirations, goals, and ambitions of our people.

Given below is a synopsis of the operating context of Sri Lanka

Despite the resilient performance following the immediate aftermath of the COVID-19 pandemic, Sri Lanka’s economic performance and outlook remain threatened due to the severe fiscal and external imbalances. The resultant political and social unrest, and the unfavorable global economic situation, have exacerbated the economic woes of the island.

The economy recovered from the pandemic-induced economic contraction in 2020, with significant contributions from manufacturing, financial services, construction, transport, and real estate activity. However, the Central Bank Governor, warned that this recovery is expected to be short-lived under the current economic crisis, with Sri Lanka having to brace up to witness the worst economic contraction in its history.

Amid the sharp deterioration in reserves, the pressure exerted on the exchange rate was ultimately reflected in an exchange rate adjustment in early March 2022, resulting in the USD/LKR exchange rate depreciating by around 80%. The economic activities of the Nation were further disrupted by the social unrest and political instability caused by regular power cuts, lengthy fuel queues, shortages of essential commodities, and escalating inflation levels. As Sri Lanka’s foreign exchange crisis worsened, the country suspended approximately, USD 25 Bn. in government external debt repayments excluding multilateral debt which is to be restructured as expected by the CBSL.

The significant tightening of monetary policy by the Central Bank led to a sharp increase in the yields of government securities leading to higher marked-to-market losses for financial institutions. The economic downturn and high-interest rate environment are likely to hurt loan growth in 2022, whilst the sharp increase in lending rates is likely to reduce the repayment capacity of borrowers amidst a depressed macroeconomic environment. The financial services sector would be required to make higher impairment provisions, that would impact the bottom-line growth.

Alongside the domestic economic recovery, Sri Lanka’s export sector recorded strong growth, with monthly exports exceeding USD 1 Bn. during the 10 consecutive months from June 2021 to March 2022, mainly driven by industrial exports. Although the recovery in exports and restrictions on non-essential imports, provided some respite to the external trade balance during mid-2021, the overall increase in global commodity prices, weak tourism income, and remittances added pressure on the current account deficit towards the end of the year. Sri Lanka entered into negotiations with key bilateral and multilateral partners for aid and financing facilities in the context of dwindling reserves and loss of access to global capital markets. Thus far, India has extended over USD 4 Bn. in financial support in 2022. Intending to ensure the sustainability of the country’s external debt for restoring macroeconomic stability, the Government and the CBSL have identified the need for implementing urgent measures and economic reforms to address external sector vulnerabilities aimed at resolving persistent and long-standing issues in the economy. Together with bilateral support, the government has commenced negotiations with the International Monetary Fund (IMF) at varying levels across April, May, and June 2022. An IMF delegation arrived in Sri Lanka on the 20 June for further discussions on a possible IMF program which is expected to be at least USD 3 Bn. spread across 3 years. An IMF program is expected to unlock additional bridging finance from other bilateral and multilateral partners. However, to secure and proceed with an IMF programme, Sri Lanka will need to implement several structural reforms including fiscal consolidation, state-owned enterprises reform, and achieve public debt sustainability.

Disruptive digital technologies gaining traction

From customer service chatbots to software robot bankers, disruptive digital technologies like artificial intelligence (AI), robotics, and blockchain are changing the financial services industry. This affects our competitiveness, and our ability to remain relevant to our customers, whilst increasing vulnerability to cyber risks.

Challenges |

Opportunities |

Impact on CDB |

Our response |

| 1. Rapid innovations from FinTechs and telcos with the challenge to integrate and up-scale digital innovations 2. Complexity of managing technology, information and cyber risks 3. Increased competition for specialised skills, such as information technology, data analytics and risk management 4. Customer behaviour influenced by disruption through FinTechs and telcos |

5. Several initiatives launched by the Central Bank of 6. Opportunities for process automation and adoption of AI to decrease cost-to-serve and enhance customer convenience 7. Customers increasingly adopting digital products 8. Automation enables to cut down on human error and improve decision making efficiency and processing speed 9. Adoption of an AI-first mindset helps to resist encroachment by expanding technology firms 10. Early adaptation of FinTech solutions enables to achieve an accelerated pace of growth 11. Digital adoption enable businesses to expand beyond geographical boundaries |

|

|

Depleting foreign exchange and heightened external sector challenges

Sri Lanka’s external sector experienced heightened vulnerabilities in 2021 amid persistently high debt service obligations and a weakened balance of payments (BOP) position along with lacklustre performance in the domestic foreign exchange market with continuous pressure on the external value of the currency.

Challenges |

Opportunities |

Impact on CDB |

Our response |

12. Slowdown in the economy 13. Currency depreciation against the US Dollar and related cost escalations in the support products and services 14. Import restrictions on motor vehicles 15. Declining worker remittances 16. Reduced rental collection and related increase in credit risk 17. Reduced profitability due to cost escalations and higher expected credit cost 18. Rating downgrades over concerns about sovereign debt sustainability 19. Increased risk due to people using informal channels (Hawala channels) to transfer funds |

20. CBSL provided incentives to remit foreign earnings through formal channels 21. Opportunities to expand local products and businesses, especially businesses engaged in import substitution 22. Positive impact on local exporters, as exports become more competitive in the international market |

|

|

Tightening Monetary Policy stance by the CBSL

The Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) were both increased by 50 basis points in August 2021, by 150 basis points each in total in January and March 2022 and by 700 basis points in April 2022. This affects our net interest margin and profitability.

Challenges |

Opportunities |

Impact on CDB |

Our response |

23. Compressing of the net interest margin 24. Impact to profitability due to mark to market adjustment of financial instruments 25. Decline in new lending 26. Increase in cost of funds negatively affecting the profitability |

27. Invest excess liquidity in high yielding government securities 28. Increase in customer willingness to place deposits due to high interest rates |

|

|

Increasing governance, social and environmental aspects

Social and climate change risk impacts our Company, our customers and the operating environment. There is an increasing regulatory, political and societal focus on the transition risks associated with climate change with tightened regulatory measures for non-compliance and increased social expectations.

Challenges |

Opportunities |

Impact on CDB |

Our response |

29. The increasing pace and evolving complexity of regulatory and statutory requirements across the financial services industry 30. Customers becoming increasingly socially conscious and the increased requirement for solutions that aid the transition to a low-carbon economy 31. Increasing severity of penalties and regulatory sanctions for non-compliance 32. Requirement for improved governance and transparency in business conduct 33. Health and safety 34. Failure to meet ESG commitments and related social expectations could lead to customer and community impacts and reduced shareholder value impacts |

35. A strong and stable financial services sector 36. Opportunities to create sustainable financial solutions 37. Opportunities to create social entrepreneurship to solve societal challenges 38. Opportunities to support small and medium businesses who are the backbone of the 39. Commitment to sustainable development goals |

|

|

Materiality

GRI 103-1, 103-2, 103-3, 203-1, 203-2, 203-3

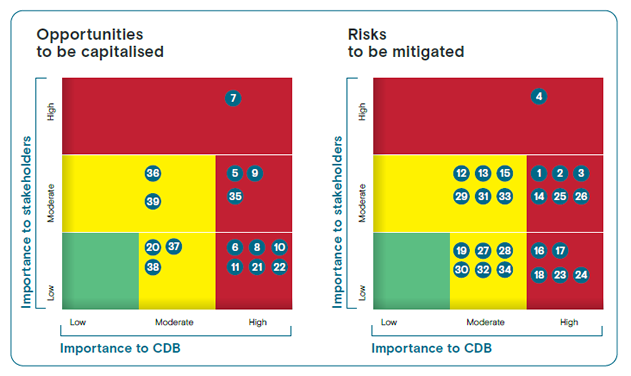

We view value creation in the needs and priorities of our stakeholders in the context of the constantly changing environment within which we operate. Accordingly, the material matters have the most impact on our ability to create value over the short, medium and long-term. These matters influence our stakeholders and our Company to varying degrees. The materiality of each matter is determined based on three aspects - its relevance, the magnitude of its impact, and the probability of occurrence. Even as the above market drivers create trends that present risks, opportunities, or both, the matrices that follow, illustrate the material topics according to their impact on our stakeholders and organisation.

Our management approach

GRI 102-47

We manage the material topics through our strategic planning process. As indicated in the table below, each material topic is linked to one or several strategic imperatives. To achieve the relevant strategic imperatives of each material topic, we have assigned responsibilities to the respective heads of divisions and allocated the necessary resources based on the significance of each material topic. To ensure achievement of the material topics, goals and targets have been embedded in the relevant KPIs with close monitoring and review at regular intervals.

Policies have been formulated to manage the material topics and to guide our people to conduct activities in a responsible, ethical, and transparent manner. These policies are duly adopted by the Board of Directors and are reviewed at predetermined intervals to stay current with the changing environment.

We have instituted formal grievance mechanisms to address and resolve grievances. Furthermore, lending to our customers and dealings with our business partners are screened for social and environmental aspects and all our internal controls, policies and procedures which are laid down to achieve the objectives of material topics are subject to internal and external auditing and verification to ensure adherence. The findings are reported to the Board and/or the Management Committees periodically for information and for corrective action where necessary. The numerous awards and accolades received by our Company over the years demonstrate the effectiveness of the management approach we have adopted.

Material aspects

GRI 102-47

Material topic |

GRI disclosure |

Stakeholder |

Strategic imperative |

| 1. Process automation and adoption of AI |  |

||

| 2. Customers increasingly adopting digital products | |

||

| 3. Slowdown in the economy | GRI 201: Economic performance |

|

|

| 4. Import restrictions | GRI 201: Economic performance |

|

|

| 5. Declining worker remittances | GRI 201: Economic performance |

|

|

| 6. Declining global competitiveness of Sri Lanka | GRI 201: Economic performance |

|

|

| 7. Increased credit risk defaults and lower recoveries | |

||

| 8. Relief measures introduced by the CBSL and injection of liquidity to the system | |

||

| 9. Rapid innovations from fintechs | |

||

| 10. The complexity of managing technology, information and cyber risks | GRI 418: Customer privacy |

|

|

| 11. Increased competition for specialised skills | GRI 404: Training and education |

|

|

| 12. Customer behaviour influenced by disruption through fintechs | |

||

| 13. Grow the lending portfolio | GRI 201: Economic performance |

|

|

| 14. Expand fee and commission income | GRI 201: Economic performance |

|

|

| 15. Health and safety | GRI 403: Occupational health and safety

GRI 416: Customer health and safety |

|

|

| 16. Create sustainable financial solutions | GRI 307: Environmental compliance

GRI 308: Supplier environmental assessment GRI 419: Socio-economic compliance |

|

|

| 17. Create social entrepreneurship to solve societal challenges | GRI 413: Local communities |

|

|

| 18. A strong and stable financial services sector | |

||

| 19. Commitment to sustainable development goals | GRI 307: Environmental compliance

GRI 419: Socio-economic compliance |

|

|

| 20. Support small and medium businesses that are the backbone of the Sri Lankan economy | GRI 413: Local communities |

|

Please refer Engaging with our stakeholders and Our strategy for the guide on icon used above.

Our stakeholders

Our principal stakeholder groups are those who potentially have the most significant impact on our value creation process and those who are affected most by our activities. Accordingly, the key stakeholders of CDB are investors, customers, business partners, regulators, employees, the community and the environment. The unprecedented conditions that prevailed during the year, created a need for a deeper engagement with our stakeholders to clearly identify their concerns during these challenging times. By maintaining continuous and open engagement through multiple platforms, we continued to strengthen the engagement with our stakeholders during the year. Furthermore, we are ready to play our part in rebuilding our nation offering unflagging support and empowerment to our stakeholders as a premier financial services institution.

Stakeholder mapping

Power |

|||

High |

Low |

||

Interest |

High |

Key players A very strong group with high power and interest, capable of proposing new strategies and driving change. Their decisions could have a considerable impact on CDB’s operations. Hence, we nurture strong relationships through ongoing engagement. |

Keep informed These groups have a high level of interest in the business, even though their power to exercise is low. They build a strong foundation to support the Company. Our strategy of engagement is to keep them informed and provide feedback and suggestions about our Organisation. |

Low |

Keep satisfied They exert a high power through their decisions by influencing the direction of the business environment. Although they do not exhibit a high interest in the company, they ensure Company’s compliance with relevant regulations through close monitoring. |

Minimal effort We do not have any stakeholders in this category with low power and low interest in our organisation. We continue to maintain an interest in our stakeholders in every aspect of our business. We respond to their expectations and needs as they in turn, become partners in the progress of the Company. |

|

Engaging with our stakeholders

GRI 102-40, 102-42, 102-43, 102-44

| Their concerns | How we engage | Our response and responsibilities | Method of engagement | |

|

|

|

|

| Their concerns | How we engage | Our response and responsibilities | Method of engagement | |

|

|

|

|

| Their concerns | How we engage | Our response and responsibilities | Method of engagement | |

|

|

|

|

| Their concerns | How we engage | Our response and responsibilities | Method of engagement | |

|

|

|

|

| Their concerns | How we engage | Our response and responsibilities | Method of engagement | |

|

|

|

|

| Their concerns | How we engage | Our response and responsibilities | Method of engagement | |

|

|

|

|

| Their concerns | How we engage | Our response and responsibilities | Method of engagement | |

|

|

|

|