CITIZENS DEVELOPMENT BUSINESS FINANCE PLC

ANNUAL REPORT 2021/22

Customers

GRI 103-1, 103-2, 103-3 ![]()

We create customer value by providing financial solutions to elevate their aspirations in an innovative, easily accessible and responsible way. By leveraging our digital technologies and embedding ourselves seamlessly into our customers’ lives, we deliver differentiated customer experiences by managing through journeys and ensuring our products and services are accessible and inclusive to all people. This enables us to build long-lasting customer relationships and maintain trust by safeguarding our customers’ data and information as we operate with high standards of conduct.

Delivering excellent customer service is an ethos that we will carry forward as we continue to be deliberate in adopting a customer-centric approach in every process across our Organisation.

Customer experience focus

We remain committed to ensuring that all decisions that are taken and systems implemented within our Company are fixated on customer experience. Delivering excellent customer service is an ethos that we will carry forward as we continue to be deliberate in adopting a customer-centric approach in every process across our Organisation.

Giving high priority to customers’ emotional connection with our brand, we continued to spur customer activity, elevate our brand and strengthen customer loyalty. Our interaction with customers was focused on simplicity, transparency, clarity and empathy to fulfill their diverse aspirations. The steady growth in our customer base over the years bears witness to the effectiveness of our customer-centric strategy.

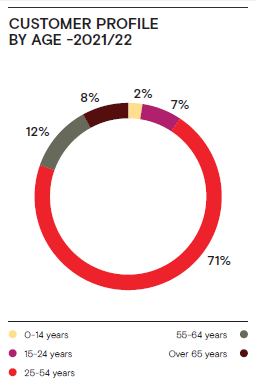

An analysis of our customer base for 2021/22

Our insight-driven customer value proposition is focused on customer lifecycle management. Even as the journey of the customer keeps evolving, we strive to forge deep relationships through a customer life cycle approach, enhance our product suite and improve access to financial services through our network combining physical and digital platforms. Whilst developing new technology-based solutions that elevate customer convenience, we also focus on strengthening customer security and privacy through state-of-the-art technology and data governance.

During the year, we made several enhancements to our processes and delivery channels to improve customer experience.

- We operated the “Doorstep” service to serve our customers at their doorstep. A range of services including delivery and collection of documents, delivery of FD certificates and savings passbooks were extended through this service, increasing customer convenience and value.

- The account manager concept was rolled out to the premier segment to provide customised service, create positive customer experiences and strengthen customer relationships. We will introduce this concept to other customer segments as well in the ensuing year.

- The CDB Flexi Capture App, which is one of the most revolutionised apps in the industry to update customer information using a smartphone in a secure environment was fully operationalised to process loan and lease facilities remotely.

- A loyalty rewards programme was launched to strengthen customer relationships further by rewarding customers for their long years of relationship with CDB. A Customers Lifetime Value (CLV) model was developed to facilitate the loyalty rewards programme.

- Customer Relationship Management (CRM) harnessed customer data to upsell and cross sell products by identifying potential business leads, converting them into sales, monitoring the progress and following up.

- To improve customer retention and loyalty, the CRM conducted several events focused on external customer satisfaction and internal customer development.

- Under the service standardisation program we have initiated the CRM set service level standards to improve customer service. This programme will include staff grooming and training to deliver an outstanding customer service.

- During the year, in addition to the Call Centre, a Service Management Unit (SMU) was set up to handle customer feedback and inquiries. This centralised unit redirects customer feedback and inquiries to the relevant department or branch, ensuring its resolution within the stipulated Service-Level Agreements (SLAs). In addition, the SMU implemented preventive measures by analysing customer feedback. Furthermore, the SMU conducts Mystery Caller programmes periodically to ascertain customer perception about the Company and service standards. The findings have helped to improve customer service levels.

- We have strengthened our customer relationships through the “Affiniti” sales app, which facilitates customer engagement in a structured and efficient manner.

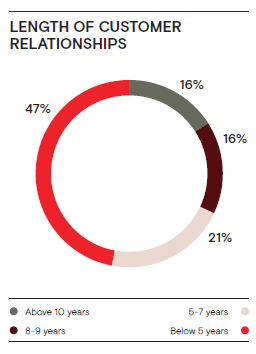

The outcome of the numerous efforts undertaken over the years to improve customer experience has resulted in long-standing customer relationships. Close to 53% of our customer relationships extend over five years.

Digital transition increasing customer acquisition

GRI 102-6

We provide pioneering solutions that make transacting simpler for all segments of the population. Customers continued to use digital solutions increasingly for simple transactions, saving time and reducing unnecessary visits to a branch or calls to the contact centre. We further enhanced the value by making customer onboarding process more simplified and efficient through the CDB Flexi Capture App given to our field-based marketing staff facilitating mobile phone enabled document submission and Robotic Process Automation (RPA) based data entry through the Optical Character Recognition (OCR) and Intelligent Character Recognition (ICR) options. The entire process of granting credit facilities to customers has been automated, reducing the credit process lead time significantly from approximately four days to one day. The end-to-end automation includes customer onboarding, savings account opening, issuance of debit cards, Application Programming Interface (API) based checking of CRIB reports, file submission through CDB Flexi Capture App, Enterprise Resource Planning (ERP) based credit facility approval and delivery of digital delivery order to the customer real time.

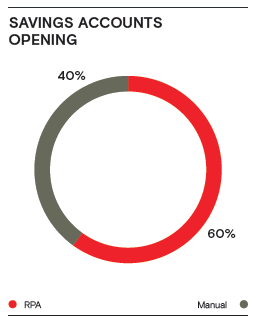

Almost fourteen thousand customers are now using our digital self-service channels, including the CDB iNet App and CDB iControl App, with over 9,000 new registrations in 2021/22. Further, during the year, more than 50,000 clients have been digitally onboarded and more than 10,000 savings account openings were done using our RPA technology. Furthermore, more than 77,000 Know Your Customer (KYC) was conducted during the year, while onboarding new customers and existing customers based on the transaction criteria whilst assuring privacy of data and adhering to all required regulations.

Digital onboarding and account opening statistics

- Average credit card requests – 865 per month

- Average credit file request – 3,513 per month

| Channel | Number of client codes | % |

| RPA | 50,417 | 89 |

| Manual | 6,417 | 11 |

| Grand total | 56,834 | 100 |

| Channel | Number of client codes | % |

| RPA | 10,995 | 60 |

| Manual | 7,339 | 40 |

| Grand total | 18,334 | 100 |

Key automations during the year

Lending process automation

Overview

In tandem with CDB’s strategic pillars of tech disruption and sustainability, we initiated an end-to-end lending process automation project to enhance accuracy, timeliness of customer deliverables, capacity improvement optimum resource utilisation and compliance. CDB pioneered this initiative among the financial institutions in

Sri Lanka, where an automated system was introduced for the credit approval process which is executed with minimal human intervention. An initial investment of Rs. 30 Mn. was made in 2019/20 on this project and it included the automation of the entire credit process including CRIB report automation, insurance debit entry automation, automated credit scoring and automated data entry process.

A cross functional team was deployed to provide oversight to the process comprising business operations, information technology, compliance, risk and credit evaluation.

Areas of improvement

- Marketing officers were enabled to check and download CRIB reports through any electronic and smart device

- Digital customer onboarding

- Credit file submission through any electronic and smart device

- Data digitalisation through OCR/ICR

- Automated credit decisions for facility approval via any electronic and smart device

- Robotic Process based data entry/facility sanctioning

- Queue management system for supplier payments

The outcome

A comprehensive Robotic Process Automation (RPA) integrated scanned image process is used for all operational functions related to credit facilities. The process which requires minimal human intervention, facilitates the sales force to work from anywhere, anytime 24x7, 365 days of the year. This process has facilitated customer onboarding from any location, and the approvals for facilities and credit cards are given through the ERP process, minimising the need for customers to visit a branch. This enables us to expand our reach beyond our physical presence specially in the rural areas with untapped markets.

The automated credit decision system which provides instant credit decisions for small ticket financing and on branch managers capacity of up to

Rs. 2 Mn. which account for nearly 70% of our portfolio, has expedited the credit execution process, reducing the lead-time.

Benefits

- Initiated a paperless working environment for credit facility approval process

- Offering a timely and faster customer service anytime anywhere

- Established 45 virtual operations units during the year. As per the strategic distribution blue print, the number of channels are being increased annually with the contribution from virtual operations improving to a level in excess of Rs. 350 Mn. per month by the year end.

- Redeployed 50 team members to attend on key processes within the Organisation

Insurance debit placement and process automation

Overview

Our Insurance Division safeguards the financial interest through active insurance policies that cover every active auto finance and property finance facility. The key deliverables include accuracy, timeliness and compliance, and the main functions of the division are insurance debit placement, policy renewal and premium settlement. Placing the insurance debit is crucial to issuing a delivery order to the customer promptly and settling the supplier payment in a timely manner.

The outcome

The Insurance Division is in the forefront of our sustainability and tech disruption strategy. The Division is fully automated, 100%

paperless and fully integrated with RPA with minimal human intervention. Our sales force is empowered to work from anywhere, anytime, 365 days of the year. The renewal entry process of insurance policies are fully automated as well.

Benefits

- Created a paperless working environment

- Contributed towards our sustainability strategy through cost savings

- Offering a timely and faster customer service anytime anywhere

- Redeployed team from

non-value adding functions

| Function | Manual | New |

| New debit entry automation | (23,263*4 Min = 93,052 Min) 1,551 Man hours | Fully automated |

| Renewal placements | (64,119*4 Min = 256,476 Min) 4,275 Man hours | Fully automated |

| Payment entries | (93,112*3 Min = 279,336 Min) 4,655 Man hours | Fully automated |

| New debit paper usage (number of papers printed) | 23,263*3 = 69,789 paper copies | 100% paperless |

| Renewal debit paper usage (number of papers printed) |

64,119*3 = 192,357 paper copies | 100% paperless |

Customer segmentation

We segment our customers to gain deep knowledge and understanding of the customer and align our product and service offering to suit their unique requirements. Our telesales unit liaises with potential customers, to convert a lead into a sale.

Catering to the life cycle of customers

We strive to enhance customer satisfaction and experience through ongoing innovation and expansion of our products and services. Our legacy systems have been replaced with next-generation platforms to reduce inefficiencies in resource utilisation to improve our customer service standards and increase customer satisfaction and loyalty. Interactions with our customers, through numerous touchpoints, provide us information to understand customers and meet their specific requirements. Our products cater to every life stage of our customers. Using technological disruption and smart financial engineering, we use our digital capabilities to create tailored customer value propositions. We also facilitate customers to evaluate real-life options, and make their lifestyle decisions through the customer life cycle.

During the year under review, we continued to integrate the sustainability agenda to the business strategy and we rolled the CDB Advance Roof Solar product to encourage customers to adopt sustainable living habits.

Our product portfolio

GRI 102-2

Our conventional and check-in product portfolio

Products catering to different life cycles of customers

Service based on the future potential of customers

We meet the aspirations of lower and middle-income segments and thereby elevate their living standards, giving them a feeling of prestige and recognition by empowering their aspirations. The “Account Manager” concept, helps to create long lasting customer relationships, offering a personalised service, meticulously attending to their financial needs and providing the best financial solutions to cater to their requirements.

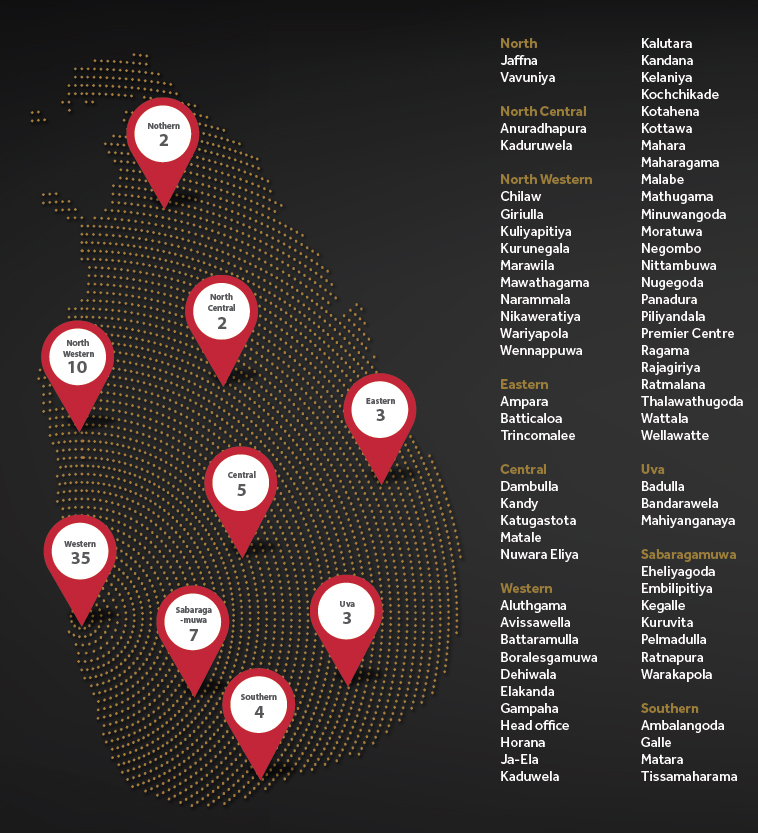

Expanding customer touchpoints

We extend financial services to our customers through a multichannel approach. There are multiple customer engagement platforms ranging from digital solutions to the call centre and face-to-face engagements through branches and relationship managers. Over the last two years, there has been an acceleration in migration to digital channels and services, by both consumers and businesses, especially following social distancing that created a surge in demand for online commerce, contactless payments and digital cash transfers. Our value proposition, “Tech with a touch” encompasses people-enabled technology. We have not opened brick-and-mortar branches over the past four years. We have continued to expand our reach through virtual operations.

ADOPTION OF OUR DIGITAL PRODUCTS BY CUSTOMERS

We aim to convert our entire deposit portfolio to iDeposits in the long term.

The CDB iControl app empowers CDB cardholders to take complete control of their credit card spend, facilitating tracking of the credit card spend with graphical data presentation, setting sublimits on spend categories to manage finances better, blocking a lost or stolen card instantly and selecting countries and merchant categories for secure payments.

The number of customers engaging with us on social media and through our corporate website has increased over the years.

Our customer touchpoint map

GRI 102-4, 102-6

An efficient call centre

GRI 418-1

The call centre which is the focal point of customer contact enables customers to make inquiries, requests, complaints, and provide feedback. The centre operates 24x7, 365 days a year, handling inbound and outbound calls and other functions. Even during the pandemic-related lockdowns, the call centre continued uninterrupted operations by working extended shifts and by working remotely, with strict compliance to safety protocols.

During the year, several enhancements were effected to augment customer experience.

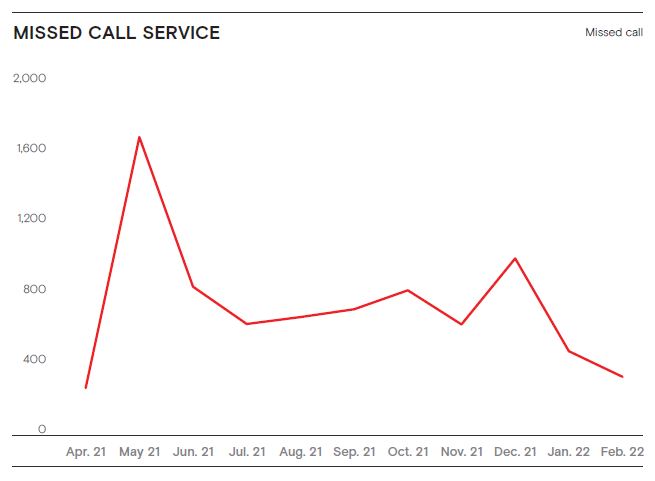

- A toll-free “Missed Call Service” was initiated at branches enabling customers to contact the CDB contact centre through a dedicated hotline. A contact centre agent would contact the customer directly for a missed call given.

- The Customer Data Retrieval Solution was modified enabling call center agents to view the summary of customer portfolio in one interface. This enabled a more efficient and speedy response to customer inquiries through easy customer verification, reduction of customer handling time and prioritising of customer segments.

- The call centre enabled lending customers to check their outstanding balance by giving a missed call to the dedicated number and receiving the outstanding balance via a SMS.

- Dedicated agents were appointed to cater to the needs of high net-worth segments to deliver specialised services.

OUR CALL CENTRE STATISTICS FOR 2021/22

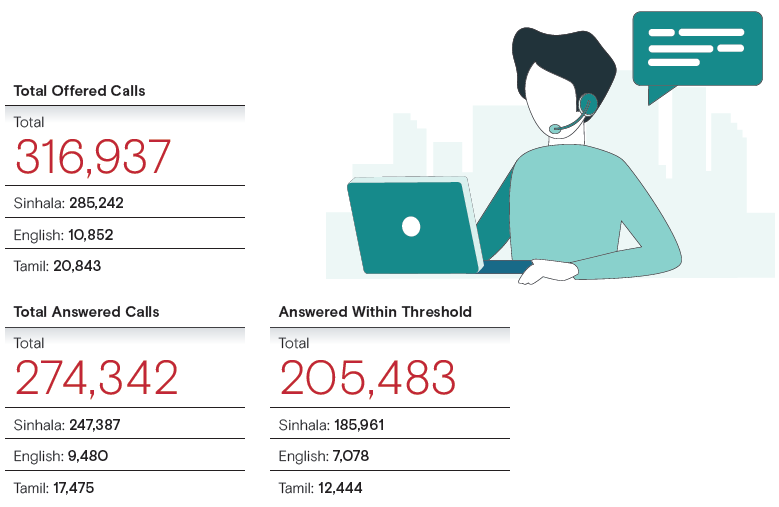

During the year under review, a total of 316,937 calls were received by the call centre of which 274,342 calls were answered and 13% of the calls were abandoned. All these abandoned calls were called back by a contact agent of the call centre as per the call-back service. A total of 205,483 calls were answered within the threshold.

Improving our brand equity

Our brand strategy is to position CDB as an innovative and sustainable brand in the banking and financial services industry. We achieve this by embracing the mindset of a disruptor and offering tech-infused smart product solutions that are environmentally sustainable whilst focusing on financial inclusion and community impact. Hence our brand intent is to “Empower a smart and sustainable Sri Lanka”.

Exemplifying the quintessence of our purpose of empowering aspirations, we etched yet another milestone by being ranked among the Top 50 of Sri Lanka’s Most Valuable Consumer Brands in 2021. We have consistently improved our brand equity through the application of the fundamentals of our core values of perseverance, empathy, reliability and innovation into our customer engagement.

Marketing campaigns, promotions, and marketing communications

GRI 206-1

Our social media strategy broadly encompasses a platform-driven content strategy that involves three strategic pillars –

- Influencer-based marketing strategy - To reach new audiences and create a greater impact on the message/campaign.

- Product-driven content strategy – To create innovative and audience-based content to improve reach and engagement.

- Customer engagement – Keep the audience engaged through numerous activities including competition.

We support our customers to make informed decisions by implementing a clear marketing and branding strategy. All our communications are conducted in a transparent manner maintaining ethical marketing practices. All relevant information in terms of products and services are disclosed in three languages (English, Sinhala and Tamil).

During the year, we improved our reach via digital marketing. Our product-focused content strategy helped to augment customer reach via social media and improve web traffic as well. We also increased our propaganda vehicle fleet from three to 10 vehicles to create more awareness of our products and services among customers.

The following campaigns were conducted during the year to promote our products among customers:

- A campaign was conducted to promote CDB Advance Roof Solar to encourage people to embrace sustainable living.

- Focused on the digital fixed deposit feature of CDB iNet, a campaign was conducted as an extension to the “Be Smart & Stay Safe” campaign to encourage people to open digital deposits with just Rs. 5,000. This campaign was to encourage youth to save for their future, in a hassle-free manner using their mobile phone or any other smart device. The content was created on Instagram and Facebook creating product appeal to the youth lifestyle as well.

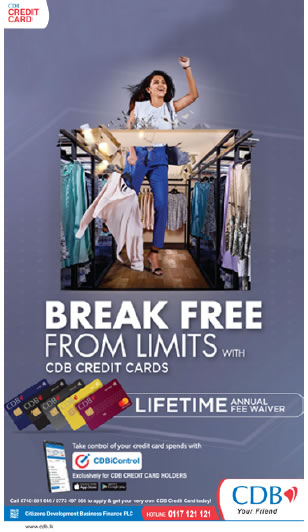

- The EMI feature was introduced to our “Break free from Limits” campaign for CDB Mastercard Credit Cards, enabling customers to purchase anything from any merchant up to 60 months instalments at 0% interest.

- Continuation of the CDB Leasing with Cash Lease and Aspired Lease campaign. As Sri Lanka is now gearing towards supporting local business and encouraging self-startups allowing especially youth of Sri Lanka to actively contribute to national GDP. By understanding the need, CDB Leasing communications were given an innovative twist in terms of bringing the national interests in supporting entrepreneurial innovation and SME support.

Especially through CDB Cash Lease campaign we encourage people to use their vehicle as an asset to finance their business or education etc. without selling their vehicle.

- Sponsoring the first ever National Cricket tournament as the Title Sponsor for Sri Lanka vs. West Indies test series in order to improve brand visibility and also to create association for the CDB corporate brand. This sponsorship was amplified through digital communications, print communications, public relations and employee engagement initiatives.

Customer privacy

GRI 418-1

We take the security of our Company, our customers and our customers’ information very seriously. Even as cybersecurity threats continue to be significant, our approach to mitigating cybersecurity risk involves a range of controls relying on people, technology and process. We have invested in state-of-the-art technology and training our team members on protecting customer information under the CBSL guidelines. Stringent information security measures are in place including, limited access, passwords, segregation of duties, data backup systems, signing of non-disclosure agreements, limited outbound mail access, and firewalls. Customer privacy has been further strengthened through the stringent purview of our Risk Management Committee, Compliance Department, and Internal Auditors. No complaints were reported with regard to breach of customer privacy or misuse of customer information during the year under review.

As a responsible business entity, our information security is ISO 27001:2013 certified for four consecutive years via TUV NORD, one of the world’s largest inspection, certification and testing organisation. Our IT operations and systems comply with the highest international standards. Establishing strong data protection and IT security environment is inbuilt in to our overall strategy. Furthermore, we have set early target timelines and action plans to be compliant with regulatory compliance, including Finance Business Act (Technology Risk Management and Resilience) Direction 01 of 2022 that addresses customer data and protection.

Mystery customer survey

The mystery customer market research technique is implemented to evaluate the level of customer service, quality, and consistency extended by the front office staff of our branch network. This qualitative research is undertaken through an observation tracker for each branch. Individual performance is assessed based on customer care, selling skills, knowledge, and interpersonal skills while Company performance is assessed based on facilities, documentation, branch ambiance, and overall aspect of CDB. During the year two separate mystery surveys were conducted at all CDB branches and the contact centre. The results were updated to an online dashboard within 24 hours for employee education, training and speedy decision-making.

Compliance

GRI 206-1, 416-2, 417-2, 417-3

The rights of our customers are protected by the CDB customer charter. During the period under review, there were no instances of non-compliance related to product and service labelling or marketing communication guidelines. Neither were any incidents of non-compliance pertaining to anti-competitive behaviour, anti-trust,

and monopoly practices as well. Further, there were no substantiated complaints pertaining to breaches of customer privacy and losses of customer data.

No incidents of non-compliance concerning the health and safety impacts of products and services were recorded.

Priorities for 2022/23

With the sharp surge in demand for remote identification services, we will integrate the video KYC solution with our website, call centre, CDB iNet app to minimise the exchange of physical documents, and serve customers from the comfort of their homes. This will also reduce branch traffic and eliminate the need for customers to visit a branch to open an account or obtain a facility. Furthermore, to enhance the quality of customer experience, we will introduce a self-service automation services to enable our credit card customers to make billing inquiries through a simple missed call. The customers will have 24/7 access to this service with no hold time and no interaction with contact centre agents. The appraisal form of lending files will be automated, and we will strive to provide better solutions to the customers through tech disruption and innovation while reducing our carbon footprint and resource usage.